Stablecoins in Unstable Times

A Deep Dive into DeFi's Largest Market

Hi All,

Below is a magnum opus on stablecoins :). 50 pages of pure Friday night bliss for the Decentralized Finance enthusiast out there.

Stablecoins in Unstable Times: https://docsend.com/view/ajcbq2dd22yunxqn

***

Sneak peak of the conclusion below for those who do not have time for the deep dive, but genuinely think the full report is a worthwhile read if you’re interested to get up to speed on DeFi’s largest market.

IN CONCLUSION: A MARKET FOR MONEY

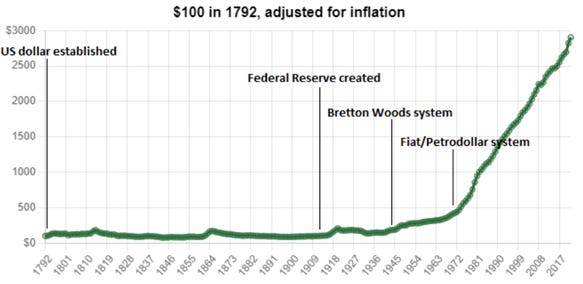

As highlighted recently by Lyn Alden, the fiat-experiment is only ~50 years old. Prior to Nixon taking U.S. dollars off the gold standard, money had gone through myriad experiments with commodity monies historically winning the day. Gold and silver in particular under-girded much of the pre-1971 financial system given their utility and broad distribution combined with rarity and relatively low “stock-to-flow” ratios (i.e. little incremental gold or silver mined annually relative to the outstanding “stock” in existence).

People act like fiat-currencies always have and always will be our units of account, but non-commodity-backed currency is a relatively young experiment, just like Bitcoin. One is backed by taxation (i.e. men with guns) and one is backed by encryption, compute power, and distributed incentives.

Obviously, correlation is not causation, but a lot of weird stuff started happening in 1971.

Without the disciplined stock-to-flow ratio of an underlying commodity like gold, fiat supply has gone parabolic over the last 50 years. Fiat still serves as a medium of exchange and “short-term” stable unit of account but has been dethroned as a store-of-value. Wealthy people are now allergic to holding cash.

US MONETARY EXPANSION

Source: Ian Webster, annotated by Lyn Alden

With CPI at ~7.9% and 10 year U.S. treasuries at ~2% , it’s easy to see why holding U.S. dollars (or any fiat) is not a great idea to protect future purchasing power.

The financially astute limit their fiat exposure to expenses and tax time while housing wealth in scarcer assets - houses, investment portfolios, fine art, gold, commodities, and real estate holdings – which hold their value against a depreciating dollar.

We already have a market for money, it’s just about to get more competitive.

DIGITAL ASSETS

Just as monies have transitioned from seashells, to stones, to beads, to gold coins, to fiat, to centralized databases with the arrival of new technologies, blockchain has introduced yet another for the digital age. The arrival of digital commodities with utility, transferability, (potentially) privacy, and scarcity. Many around the globe are electing to both transact and store their purchasing power with these new digital commodities. If gold, Rembrandt’s, and ocean-front villas appreciate relative to fiat due to scarcity, why won't a similar dynamic take place in the digital realm?

As financial repression accelerates, competition for moneyness will only increase.

In many ways, digital assets present a conundrum for liberal governments. In the industrial era, enforcing taxation was easy as asset bases and laborers were subject to national borders and regulations. The digital sphere is much less straight forward.

With the onset of COVID, white-collar workers have realized they can work from anywhere. They can collaborate on open-source software projects with distributed servers and pseudonymous teams from around the globe in the new economy. Regulatory arbitrage is increasing and smaller, more nibble governments from Singapore to Miami, Dubai to the Bahamas are competing to attract talent and capital. Portugal, Switzerland, Taiwan, El Salvador, Thailand, and Malta are just a few forward-thinking countries opening visa options for technical and financial talent.

Governments who view citizens as a revenue base to exploit will lose out to those who view citizens as customers to please.

Larger governments are stuck in a Catch 22. They can 1) clamp down on digital assets (enforceable only through mass internet censorship and surveillance incompatible with liberal ideals) and push talent and capital to more lenient jurisdictions or 2) embrace crypto, but risk continued degradation of monetary policy tools, realizing some citizens will choose to store wealth in non-censorable assets.

The middle ground - favored by most jurisdictions today - is to allow digital asset exchange, but to tax and regulate their ascent.

Easier said than done.

Sure, fiat-backed currencies like USDC can be regulated and brought to heal under existing banking and securities laws, but what about crypto-backed stablecoins? What about algorithmic stablecoins? What about "stablecoins" like OHM which don't even pretend to be pegged to any fiat-currency?

This is a bottoms-up phenomenon, based on free people, making free choices.

The likely outcome of the Cambrian explosion of stablecoins is a divorce from U.S. dollar pegs and therefore U.S. monetary policy - due to regulatory threats or catering to users afraid of the looming financial repression. If faced with a choice of a government-controlled currency with a guaranteed loss of purchasing power or an encrypted inflation-resistant currency, many users may opt for the latter.

What if merchants also prefer it? How about other nation states?

The reality is 99% of these monetary experiments will fail. However, a select few will thread the needle; constructing a medium of exchange, a stable unit of account, AND a store of value. (It's much easier to achieve when you are not saddled with ~US$300 trillion in outstanding debts.)

Governments will face a difficult question: do we implement capital controls and internet censorship or allow for open competition, innovation and risk a loss of monetary sovereignty?

Emerging markets will be the first countries to encounter this conundrum. Stablecoins - mostly denominated in U.S. dollars - present an opportunity for anyone with an internet connection to hold their purchasing power in U.S. dollars. Surely, when the alternative is the Argentinian peso, the Venezuelan bolivar, or the Russian ruble, the value proposition is compelling. This is the biggest risk expressed by the Reserve Bank of India, a country of 1.4 billion citizens.

In a world where foreign citizens have easy access to U.S. dollars, a further dollarization of the world is likely, reducing foreign governments monetary sovereignty. U.S. dollars are simply better stores of wealth than pesos, bolivars, rupees, or rubles.

As Balaji has pointed out, many smaller countries - like El Salvador - may find it better to adopt a neutral algorithmic money like Bitcoin as the reserve standard as opposed to being subject to a larger nation's (the U.S. or China) monetary policy.

Many foreign governments today are heavily dependent on the Fed: when the dollar increases in value, it becomes a wrecking ball through emerging markets with high U.S. dollar denominated debts. When the U.S. government drops helicopter money to its citizens, foreign U.S. treasury holders are forced to stomach the "dilution" without any of the gains.

During the initial phase of crypto adoption, it's easy to see an accelerating dollarization of the world - as more citizens abroad have access to U.S. dollars on-chain for the first-time. Over time, however, even the mighty U.S. dollar will be challenged.

The U.S. GDP relative to the world total is capping off a 70-year decline. China has usurped the U.S. as the world's leading trading partner. The Fed's debt monetization is accelerating. The Triffin Dilemma accurately predicted that one country's reserve currency will artificially inflate demand, making exports less competitive, and lead to large trade deficits. While reserve currencies are sticky, the fall of each is pre-destined.

THE FUTURE BELONGS TO THE INTERNET

Ray Dalio's magnum opus - The Changing World Order - details the variables which lead to an Empire's rise and fall. In his latest, Dalio forecasts the ascent of China at the expense of the United States. However, Dalio's analysis has a gaping hole. We are in an exponential age where networks are challenging hierarchies. Money is unlikely to be spared.

I prefer Parag Khanna's prognosis : "the 21st century does not belong to China, the United States or Silicon Valley. It belongs to the Internet".

The same forces that swallowed traditional media companies and information networks are coming for finance. Composable, open-source software with super-charged financial incentives is just getting started. The flywheel of capital, talent, and open-source libraries will only accelerate. It's unlikely traditional financial institutions will stand the onslaught.

Financial services are going digital, starting with money itself.

We already have a market for money. Investors jump from currencies, to stocks, to bonds, to art depending on what is likely to preserve purchasing power. Crypto simply opens the design space. As more assets come on-chain, these exchanges will become programmatic, automated, and instantaneous. Balaji calls this the "DeFi Matrix" where all assets can be exchanged in real time with any other asset. Blockchain will bring deep liquidity to previously illiquid markets.

It's only fair to assume digitally native currencies - with immutable, transparent monetary policy, optimized for stable purchasing power and enforced not by guns but by math - will be in competition. Some of them will be pegged to national currencies and regulated. Some will not…

Governments will ultimately be faced with the tough decision: to embrace the next generation of the internet and a loss of centralized power or to prove isolationist in the digital age - not dissimilar to information networks of the last 30 years.

The key difference is governance will not be subject to unelected founders and corporate board rooms in Silicon Valley and New York, but baked transparently into the protocols themselves - either immutable or governed by the users. Adoption can be forced from the top down (a la CBDCs) or elected from the bottom up (a la Bitcoin or Terra). One strikes me as less dystopian.

Stablecoins are a novelty today; a drop in the bucket against the ~US$300 trillion in debt outstanding. But what about 10 years from now? In 2032, what will be possible using opensource primitives in the digitally native financial institutions to come?

Stablecoins are just the first step.

***

Again, if you are keen to read more, the full report can be found below:

Stablecoins in Unstable Times: https://docsend.com/view/ajcbq2dd22yunxqn