Inflation vs. Debasement

DIGITAL COMMODITIES & Crypto's "DE-COUPLING" from the NASDAQ

I’ve had a few investors reach out asking about crypto’s status as “an inflation hedge” so wanted to pen my thoughts. Today, crypto serves as a hedge against the debasement of fiat, but not as a safe-haven to protect against inflation (yet). (Shoutout to Raoul Paul for highlighting the nuance)

I’m hopeful the Ethereum “merge” set for Q3 may serve as a catalyst for institutional investors to reconsider the classification of these digital commodities and break today’s high correlation with the NASDAQ.

We will see in H2…

Twitter: @PonderingDurian

There is a common misconception today regarding crypto and Bitcoin specifically as an “inflation hedge”. Inflation is running rampant (hitting a 40 year high) and BTC and ETH are down ~55 - 60% from the highs and sporting a >0.8% correlation to the NASDAQ?

What gives?

Where is my “InFlaTIon hEDgE” ser?

I’m going to posit crypto was never actually an inflation hedge, at least not yet. Crypto is a hedge against the continued debasement of fiat-currency. A call option on becoming a new reserve currency or type of digital commodity, but not yet there. The nuance between inflation and debasement is small, but important.

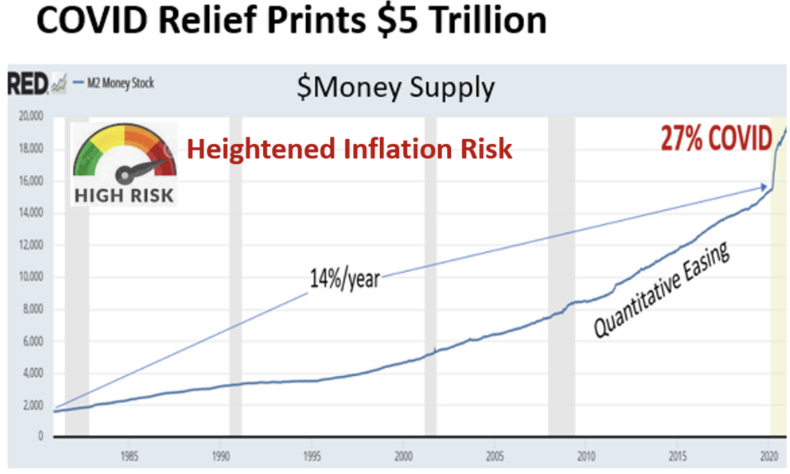

The market is forward looking and inflation is a lagging indicator. Inflation is a consequence of monetary and fiscal policy (and supply chain) actions historically. Today’s inflation rates >8% (probably >10% without housing adjustments) is a consequence of the US$13T in spending over the last two years (US$5.2T for COVID relief, US$4.5T for QE, and US$3T for infrastructure). A staggering ~65% of US GDP and a ~27% increase in the M2 money supply…

That is a lot of new dollars. The value of the dollars issued prior to this spending spree should be quite diluted.

While clearly accelerating post-COVID, increases in the money supply is not a new phenomenon. Growing at ~14% per year and accelerating post 2008, the increasing money supply has had a relatively muted effect on CPI inflation.

Source: Ron Surz, Nasdaq contributor

When the Fed prints trillions and kicks the Fed funds rate down to zero, inflation will occur. The same assets and services and more dollars = higher prices.

However, depending on who has access to the new funds, the higher prices will show up in different areas of the system.

Asset Inflation vs. CPI Inflation

2008 was primarily a subprime mortgage and credit crisis meaning liquidity went to financial institutions to ward off a credit collapse. However, despite the QE, the velocity of money did not pick up materially. Being risk averse, banks and credit markets used their artificially cheap funds to service proven, high-end customers and blue-chip corporations. The funding did not flow to goods and services but flowed into asset prices - stoking the bond bubble, stocks, mortgages for new homes, cheap credit for stock buybacks, etc.

The inflation caused by new money post-2008 showed up in financial assets.

COVID was different. With COVID, the federal government paid >US$1T in direct relief checks and ~US$900b in unemployment to the Average Joe to get through lockdowns. Sure, some of this money went into assets (see meme stocks), but much of it went to make ends meet: electricity bills, rent, groceries, etc. US$2T in new money vs. not stagnating supply, but DECLINING supply of everyday goods in the face of supply-chain issues and a war between two of the world’s leading commodity producers.

This brings inflation in Core CPI.

So, in short:

Printing money and debasing the currency = crypto (and other risky assets) goes up vs. the diluted dollar

Debasing currency ≠ always equal inflation (at least in the core CPI sense)

Inflation in core CPI = a likely future increase in the price of fiat (the opposite of debasement) to tame inflation

Increase in the price of fiat = fiat as a better relative store of value vs. competitors

Core CPI inflation is a lagging indicator of currency debasement but a leading indicator for financial tightening, which is why competing “monies” or “store of value” assets are depreciating against the dollar now.

Inflation hedge today vs. a “call option” on becoming an inflation hedge tomorrow

Monetary instruments like Bitcoin are more of a hedge against currency debasement and less of a hedge against inflation (for now), because inflation is a leading indicator of tightening financial conditions.

Bitcoin is not digital gold yet. It is effectively a call option on becoming digital gold. It might not happen. The code may have a flaw. Adoption may stall. Competing digital “monies” may usurp its position. All of these risks need to be discounted… and they are now being discounted at the increasing cost of money… leading to a decrease in the price you are willing to pay today for that call option…

ETH is similar. Ethereum is not the decentralized world computer yet. It is effectively a call option on becoming the winning decentralized world computer. It may prove to be “Myspace”. The platform may not scale. The “merge” could be botched. The majority of value may accrue to “Layer 2s”. There’s still a lot of questions. All of these questions require a discount rate. And that rate is going up…

The Merge as a “DECOUPLING” Catalyst

Because of these risks, the market is still pricing BTC and ETH like high-risk growth stocks with a correlation to the NASDAQ >0.8. Overtime, I suspect this correlation will breakdown as the market realizes BTC and ETH are maturing digital commodities: with price governed by scarce supply and increasing demand as opposed to cashflows. Historically, in a high inflation environment, scarce commodities do serve as a solid inflation hedge.

But how does this transition happen?

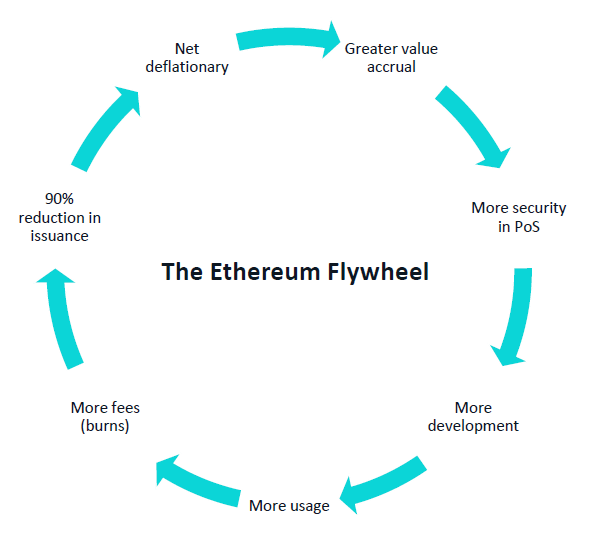

The key catalyst on the horizon to force investors to re-evaluate their investing classification is the Ethereum merge - expected (best guess!) in late Q3. Under this transition, Ethereum will move from Proof-of-Work to a Proof-of-Stake consensus mechanism. Without going into the underlying mechanics, this move will see a dramatic decrease in the new issuance of ETH (~90% reduction in sell pressure).

Rewards will no longer go to miners who are forced sellers to pay for hardware, electricity and other operating costs. Instead, rewards will go to holders of ETH who “stake” their tokens. In several estimations, new issuance on Ethereum in 2021 equated to ~US$30m daily. US$30m in sell pressure the market has to absorb DAILY. Post-merge, that figure will drop to ~US$3m. Similar to oil, a dramatic reduction in issuance should lead to an appreciating price for an in-demand commodity.

However, it doesn’t stop there. Post-merge Ethereum will have a further benefit. Stakers will receive an ~8 - 11% APR (again, best guess) denominated in ETH - a useful digital commodity which (after EIP-1559 “burns”) is likely to go net deflationary in the future.

So… to re-hash the ETH exposure post-merge… Perpetual rewards, paid out daily, equating to a ~8 - 11% APR in a deflationary currency, in a world where M2 increased by 27% last year, in the form of a scarce digital commodity which powers the rails of an exponentially growing open-source financial system (not to mention NFTmania and other use cases), and attracting developer talent in droves, in a stagflationary world where growth is hard to come by…

I’m not sure how to classify this asset, but it seems like something I want exposure to in a tough macro environment…

Yield? → YES (8 - 11% APR)

Store of value? → YES (Monetary policy substantially less inflationary than fiat)

Increasing Demand? → YES (~30m Metamask users vs. internet base of ~5b smart phones)

Catalyst? → YES (90% reduction in issuance post merge, equivalent to 3 bitcoin “halvings”)

New buyers? → YES (Proof-of-stake substantially reduces electricity making it much more palatable to ESG-aligned institutional capital)

There is a real case after “the merge” is de-risked, ETH should trade more like an “ESG-friendly, internet bond” vs. a high-risk tech stock with payments in the form of a scarce digital commodity.

This only really applies to BTC and ETH with more sustainable, deflationary economics. I fear the long-tail of risk-assets in crypto are doomed to only be bailed out by a “Fed Put”; a reversal in monetary policy once the narrative shifts from “inflation is intolerable” to “growth has fallen off a cliff, we are definitely heading into a recession”. In an inflationary regime, the “decoupling narrative” is likely reserved for blue-chip crypto assets without inflationary issuance schedules outstripping even that of fiat.

Supply and demand.

+ INSURANCE: DIGITAL BEARER STATUS

Incrementally, both BTC and ETH have the added benefit of being digital bearer instruments. As opposed to stock exposure, (which can also serve as a hedge against currency debasement), crypto is not built on the rails of the traditional system. The precarious house of cards which is the U.S. treasury market. The financial claims on assets today dramatically outstrip the underlying assets themselves. In a rapid deleveraging, the “assets” you thought you had are unlikely to materialize in whole, leading to a scramble between creditors to salvage the crumbs. With BTC or ETH, the provenance of the digital commodity is known, and in the case of ETH, has real utility in the form of distributed compute access in a world that is almost certainly only going to accelerate further into the digital domain and away from centralized intermediaries.

I don’t have a crystal ball. I’m not sure when the market will catch up and realize digital commodities are probably better stores of wealth in an inflationary macro backdrop than even physical commodities (as they are set to ride an exponential S-curve of adoption to boost demand in contrast to the algorithmically constrained supply).

But the merge is probably the brightest flashlight possible to shine these novel attributes into focus for large pools of capital scrambling to find an asset class to protect future purchasing power and reconsider the classification of digital commodities.

Based on the current price trajectory, this re-evaluation is far from priced in.